Complex factors behind gold price fluctuations: tariff policy and Chinese market demand

- February 11, 2025

- Posted by: Macro Global Markets

- Category: News

People tend to use simple narratives to explain the rise and fall of assets, but the truth is often far more complicated than it seems. MarketWatch columnist Mark Hulbert recently wrote an article analyzing the relationship between gold prices and US tariff policies.

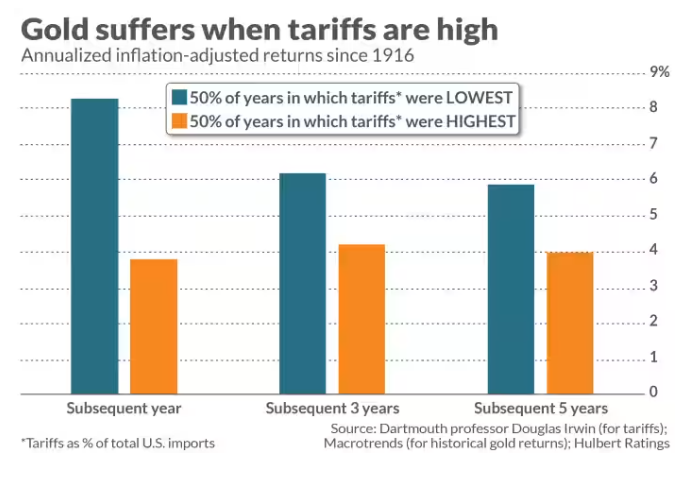

Historically, gold has underperformed when tariffs are high. This finding nicely counters the current widely held view that “high tariffs are good for gold.” To be sure, gold has been on a strong bull run as tariff threats have escalated in recent months—surging to nearly $2,900 last week for the first time ever. Gold prices are up nearly 10% since the start of the year and nearly 45% over the past 12 months.

However, it may be a mistake to attribute gold’s recent gains to tariffs. Historical data suggests the opposite may be true. To test this, Herbert analyzed data since 1916, dividing all years into two groups based on average tariff levels: above the median and below the median. The average tariff is measured as a percentage of total imports and the data comes from Douglas Irwin, an economics professor at Dartmouth College. For each group, Herbert calculated the average inflation-adjusted return of gold over the subsequent one, three, and five years (data from MacroTrends). The results are shown in the figure below, and gold generally performs better in periods of low tariffs.

However, some caution is needed in interpreting these results. First, gold was not fully freely traded until the early 1970s, when President Richard Nixon formally ended the gold standard. In addition, the chart shows that the “tariff regime” has changed relatively little in U.S. history, which makes the correlation between tariffs and gold prices difficult to determine. For example, since the early 1970s, the price of gold has risen from $35 to nearly $2,900 per ounce, but the average tariff level has barely changed. Tariffs have been below 3% of total imports for the past 30 years and have never been above 5% in the past 50 years. This is also why Herbert tried to measure the correlation between gold and tariffs over a longer time frame, not just the past 50 years.

Moreover, as statisticians remind us, correlation does not equal causation. Dartmouth’s Irwin noted in an email that before the 1960s, most tariffs were “specific” — a fixed amount per unit of imported goods, rather than a percentage. So when tariffs were expressed as a percentage of total imports, tariffs before the 1960s were generally negatively correlated with import prices (and perhaps economic activity). So we need to be open to the possibility that any simple correlation “tells us nothing.”

These complexities mean that we cannot confidently assert that tariffs are unequivocally negative for gold. But equally, this does not mean that high tariffs are necessarily positive for gold. In summary, while people tend to use simple narratives to explain the rise and fall of gold (or any asset), the truth is often more complicated than it seems. Keep this in mind when you are encouraged to buy gold because of high tariffs.

Chinese buyers may be scared off again by high prices, but one big buyer continues to support market sentiment. Chinese buyers may be scared off again by high prices as gold prices soar to near $3,000 an ounce. One of the main drivers of gold’s rise over the past year has been Chinese demand. But record prices and extra costs from a stronger dollar have made purchases too expensive for many consumers in China, the world’s largest importer.

Gold prices have been spurred by investors seeking safe havens after Trump took office as president to avoid the potential impact of the new administration’s more confrontational foreign policy. That includes the prospect of a trade war between the U.S. and other countries, which has lifted the dollar and made gold more expensive. “It’s an affordability issue… consumers can’t open their wallets or purses like they used to,” said Philip Klapwijk, general manager of Precious Metals Insights Ltd. in Hong Kong.

It also suggests that the global rush for gold could send prices higher if Chinese buyers step in. But the demand boost that usually comes ahead of the Lunar New Year gift-giving season has been smaller than usual, providing some respite for the red-hot market, Klapwijk said. While Chinese consumers’ investment in bars and coins remains strong, jewelry sales account for a smaller share of demand.

“Domestic savers may prefer gold, which is simple and relatively transparent,” said Nicholas Frappell, global head of institutional markets at ABC Refinery in Sydney. “But given the constraints of households, I don’t expect any surprising moves.” Meanwhile, wholesalers are also withdrawing less goods from exchange inventories than usual. Fenny Zeng, founder of Shenzhen Royer Jewelry, said: “People are cutting back on spending. More and more people like small jewelry with better designs.”

China’s wholesale demand for gold remains tepid. As a major importer, Chinese gold buyers often have to pay premiums for gold bars. But for much of the past six months, the Shanghai premium has actually turned into a discount, suggesting weak demand for physical gold as prices have soared.

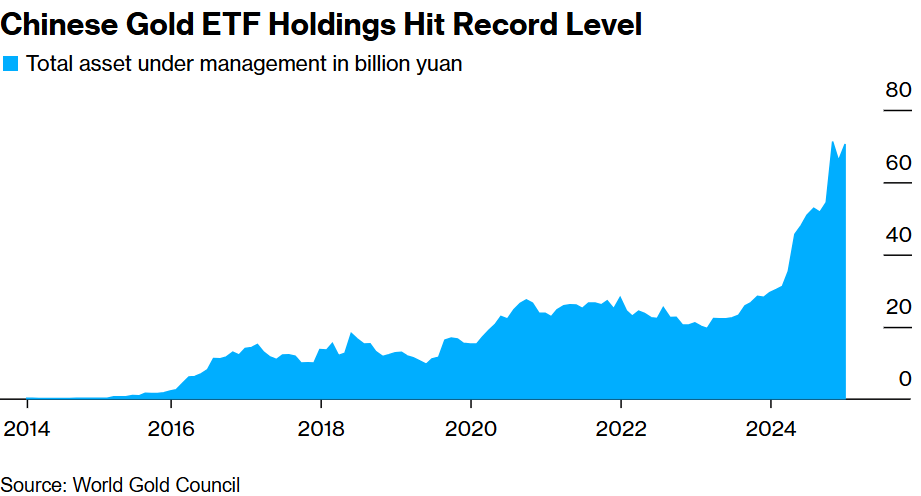

Paper gold investing, however, is another story, with gold-backed exchange-traded funds (ETFs) rising to record levels. Chinese gold ETF holdings hit a record high. In addition, there is one big buyer that continues to support market sentiment. After a six-month pause, China’s central bank resumed gold purchases in November last year as it seeks to diversify its reserves, and increased purchases in January this year, according to the latest data last Friday.