Federal Reserve meeting minutes release divergent signals of interest rate cuts, gold market seeks direction in policy game

- July 10, 2025

- Posted by: Macro Global Markets

- Category: News

1、 The minutes of the June meeting revealed differences among decision-makers, and the expectation of a July interest rate cut cooled down but did not disappear

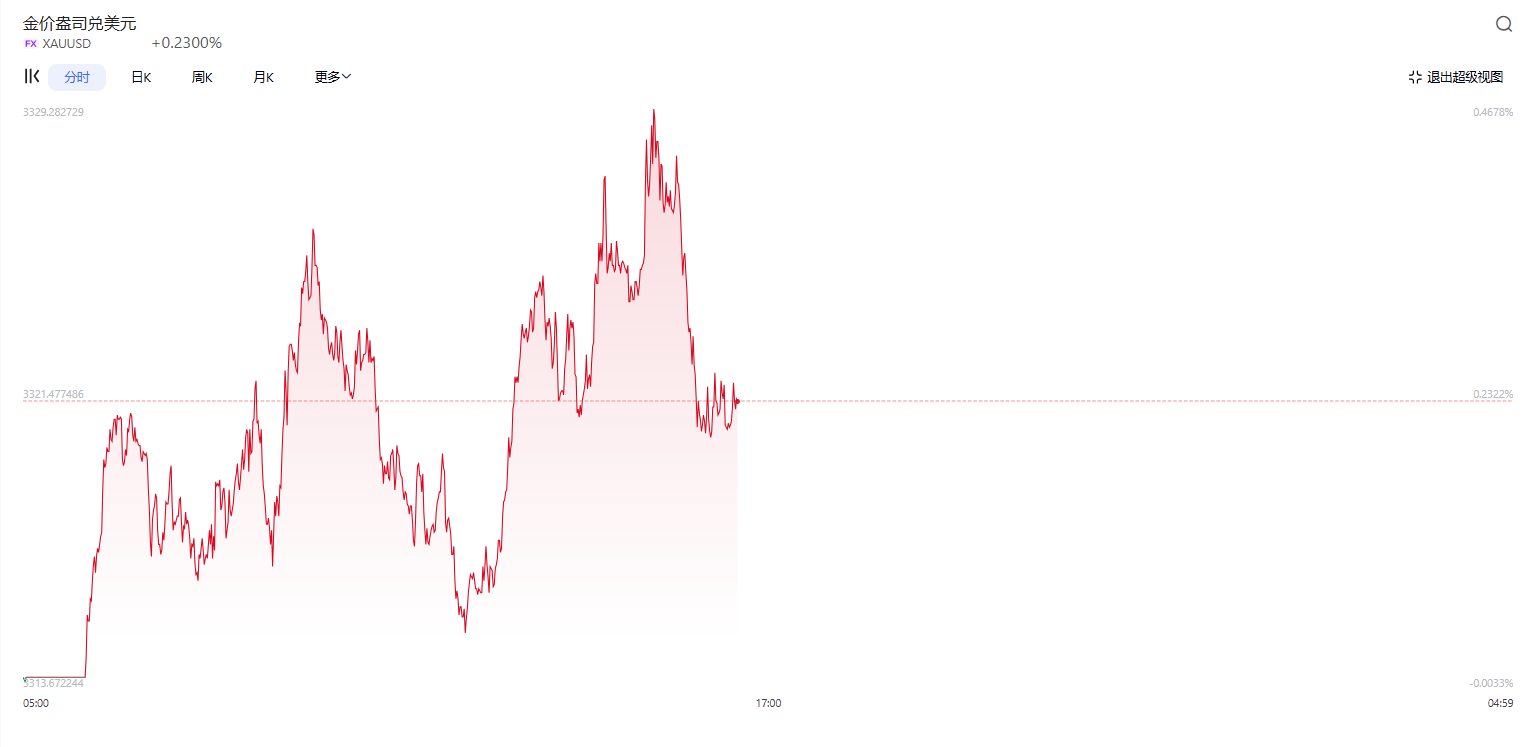

On July 9th local time, the Federal Reserve released minutes from the June 17-18 Federal Open Market Committee (FOMC) meeting, showing that some officials support considering a rate cut at the July 29-30 meeting, but most officials believe that more economic data needs to be awaited to assess the impact of tariff policies on inflation. This statement contrasts with the strong expectations of the market for a rate cut in July, leading to a volatile pattern in gold prices in the Asian market early on July 10th – London gold surged to $3326.16 per ounce at one point, then fell back to around $3318.

2、 The core logic of decision-making divergence: the uncertainty of tariff transmission and inflation path

The meeting minutes show significant differences among Federal Reserve officials regarding the impact of tariff policies. Some officials believe that the tariffs imposed by the Trump administration on imported goods may drive up inflation through supply chain transmission, but if trade negotiations make progress, this impact may be short-lived. For example, the 20% -50% tariffs on countries such as Brazil and the Philippines will take effect on August 1st, which may directly push up the prices of key raw materials such as copper and semiconductors, thereby affecting manufacturing costs in the United States. However, most officials emphasize that current economic data, such as higher than expected non farm payroll employment in June and a rebound in service sector PMI, indicate that the US economy remains resilient, and premature interest rate cuts may weaken the Federal Reserve’s policy space to address future risks.

It is worth noting that Federal Reserve Chairman Powell’s public statements after the June meeting echoed the meeting minutes. He pointed out that if it weren’t for tariff policies, the Federal Reserve might have initiated a cycle of interest rate cuts, but currently needs to balance trade uncertainty and inflationary pressures. This “wait-and-see” attitude was reflected in the meeting minutes -10 out of 19 officials expected to cut interest rates at least twice this year, but 7 believed there was no need for a rate cut, and 2 only supported one rate cut.

3、 The bidirectional effect of expected interest rate cuts on the gold market: short-term pressure and long-term support coexist

The gold market reaction on July 10th reflects the complexity of policy games:

Short term suppression effect: The market’s expected probability of a rate cut in July has decreased from 55% before the release of non farm payroll data to around 40%, leading to short-term pressure on gold.

Long term positive factors: The global trend of central bank gold purchases remains unchanged – the People’s Bank of China has increased its holdings of gold for 8 consecutive months, with reserves reaching 73.9 million ounces as of the end of June; According to data from the World Gold Council, in the first half of 2025, global gold ETF inflows reached $38 billion, with holdings increasing to 3615.9 tons, reaching a new high since 2020. In addition, the expansion of the US fiscal deficit (expected to increase $3.4 trillion in debt through Trump’s tax cuts) and the weakening of US dollar credit (with the US dollar index falling 10.7% this year) remain structural supports for gold.

The policy divergence revealed in the minutes of the Federal Reserve meeting has plunged the gold market into a game of short-term volatility and long-term optimism. Despite the cooling expectation of interest rate cuts in July, structural factors such as global trade tensions, central bank purchases of gold, and weakened US dollar credit still provide support for gold.