The market is “blunting” to Trump’s tariff policy. Gold’s safe-haven attribute hides strategic opportunities

- February 25, 2025

- Posted by: Macro Global Markets

- Category: News

Event-driven: The marginal pricing effect of tariff policy is declining

The impact of the Trump administration’s recent tariff threats on the global capital market has shown a significant blunting effect. Although policy uncertainty still exists, the market volatility index (VIX index) has fallen from 22 at the beginning of the year to around 15, indicating that investors’ immediate response to trade frictions has weakened.

In cross-asset performance, the MSCI Asia Pacific Technology Index has risen by 18% this year, and the European STOXX 600 Industrial Index has hit a seven-month high. The trend of funds migrating from safe-haven assets to risky assets is obvious. State Street Global Research pointed out that the contribution of the trade war to stock market volatility has dropped from 38% at its peak to less than 2%, reflecting that the market has digested policy shocks through the risk repricing mechanism.

Market structure: risk preference shift and liquidity trap looming

Current market sentiment presents “selective optimism”: investors shift policy focus from tariffs to Trump’s promised tax cuts (corporate tax rate may be reduced to 20%) and energy industry regulation deregulation, pushing the S&P 500 index risk premium to 4.2%, close to the lower limit of the ten-year average.

The US dollar index fell below the 102 mark, non-US currency volatility converged simultaneously, and the 30-day implied volatility of the Canadian dollar fell to 8.5%, a year-low. However, the Westpac model warns that current asset prices only reflect about 35% of the potential tariff impact. If the intensity of policy implementation exceeds expectations, it may trigger a sharp rise in risk premiums and liquidity stratification.

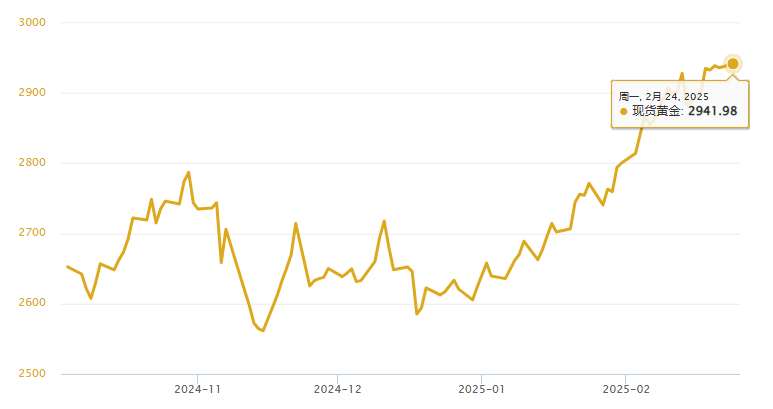

Gold logic: revaluation of the value of compound safe-haven attributes

Under the appearance of policy disturbance blunting, the safe-haven value of gold is undergoing a structural upgrade:

.Real interest rate environment support: The 10-year TIPS yield fell to 1.45%, a new low since September 2023, and the actual cost advantage of holding gold continued to expand, driving global gold ETFs to net inflows for five consecutive weeks.

.Currency credit anchoring function: The proportion of US dollars in global central bank foreign exchange reserves has dropped to 58% (the lowest since 2000), and the proportion of gold reserves has risen to 15.2%. China and India increased their holdings by 21 tons and 18 tons respectively in January, strengthening the “de-dollarization” hedging value of gold.

.Volatility cross-asset hedging: The 90-day correlation between gold and the S&P 500 index has dropped to -0.38. When the equity volatility (VIX) exceeds the 20 threshold, the hedging effect of gold is nonlinearly enhanced.

Market outlook: Tactical window under the expectation gap game

The current market’s “adaptive blunting” to tariff policies is actually a reflection of insufficient risk pricing. Natixis portfolio manager Jack Janasiewicz pointed out that there is a “gap between words and deeds” in Trump’s policies. If the intensity of the tariff list in April exceeds expectations, it may still cause market fluctuations, thereby pushing up gold prices.

For gold prices, market complacency and a weak dollar provide potential upward momentum. Investors need to remain vigilant and pay close attention to policy trends to respond to possible market changes.